Global markets have sold off pretty hard to start the week. Most of the narrative surrounds the Chinese property market and one of their largest developers, Evergrande. China’s government is clamping down on leverage and demanding many industries to buy in, literally, to their social objectives via cash “donations”, cheaper housing, etc. Both the Shanghai and Hong Kong indices have sold off quite a bit over the last few months as a result of this. At T&T Capital Management, we don’t have any significant exposure to these Chinese developers or the Asian regional banks that could likely be impacted. Remember, we have been harvesting profits and creating conservative positions using options, because we believe these markets are very frothy. Individual stock selection and strategy are going to be more important than ever, just like we saw in the early 2000’s.

The volatility index has risen quite substantially, which is very attractive for selling options, so hopefully we’ll be able to take advantage of that development. Higher volatility allows us to collect greater premiums. As your regular reminder, the impact on existing positions is often a short-term mark to market loss, but the full protection of the strategies is exhibited upon option expiration. At option expiration, both time value and volatility value go to zero, and the only thing matters is where the stock is at relative to our options strike prices. Many of our options are 15-50% below current prices, depending on the stock. We also have a multitude of covered calls sold, which provide additional income and hedging. This volatility is also very good for the big U.S. banks and their bond and stock trading businesses. I think we have a huge opportunity in several of our largest investments to close the year out strong, as I believe they’ll have strong 3rd quarter earnings releases in a few weeks and good guidance.

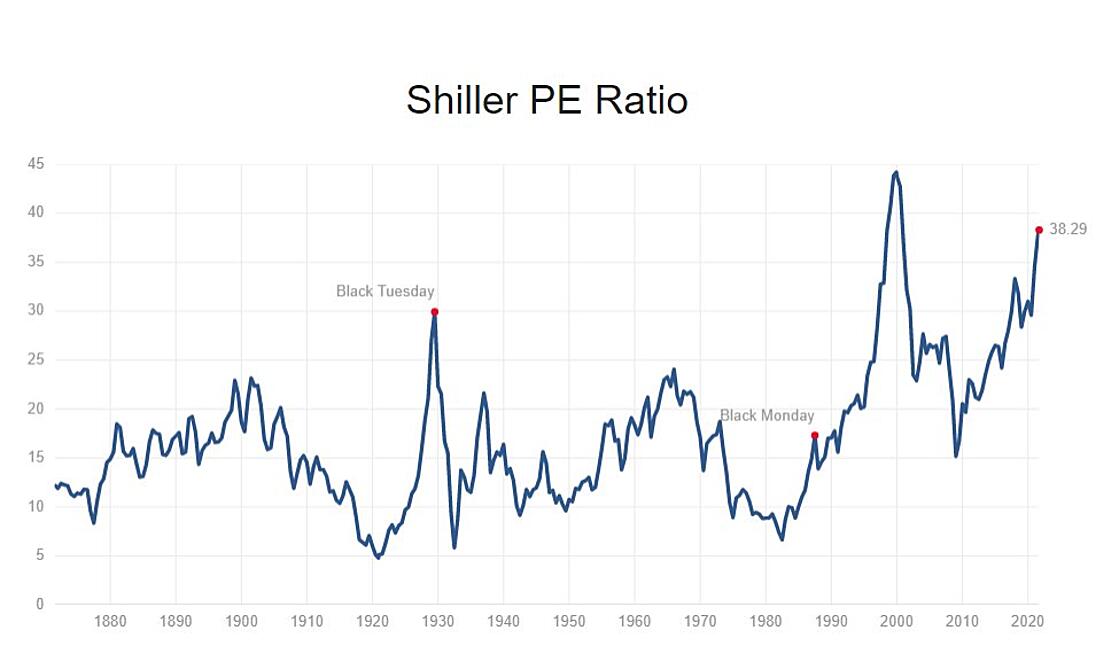

The chart at the top of this page shows the S&P Shiller or Inflation-Adjusted P/E Ratio. As you can see, it is the second highest in history. While it currently stands at 38.29, I’d like to highlight that many of our largest positions trade at P/E’s of 6-13 times, so about 1/3rd of the levels of the index, all with strong prospects over the next few years to expand those ratios and earnings. I believe a lot of market participants will be exposed over the next 3-5 years that have benefitted from this steep climb in valuations, particularly amongst the glamorous sectors. Many investors have zero qualms paying 10 or 20 times sales, which is something we’ve only seen really occur at length during the Tech Bubble, where the Nasdaq ended up imploding by 80%. As always, it is imperative to take a business-like approach to investing. If you simply chase whatever is hot, you end up getting caught in the Bubble. We saw that earlier in the year with the SPAC sector and I think we’ll see it with quite a few others moving forward. The difference in getting caught in a bubble, versus a normal correction or bear market, is that prices can take many years, if not decades to get back to even. We want to avoid that like the plague and instead focus on maximizing long-term risk-adjusted returns. Risk-adjusted is defined by avoiding permanent losses of capital. Buying the index at current levels is totally unappealing in my estimation.