|

|

|

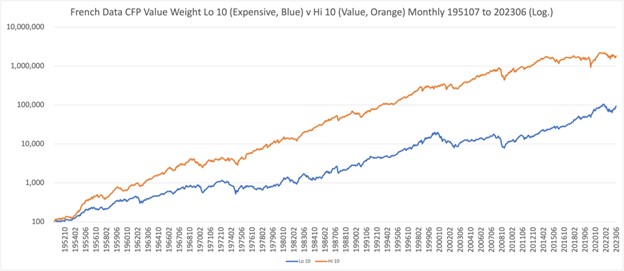

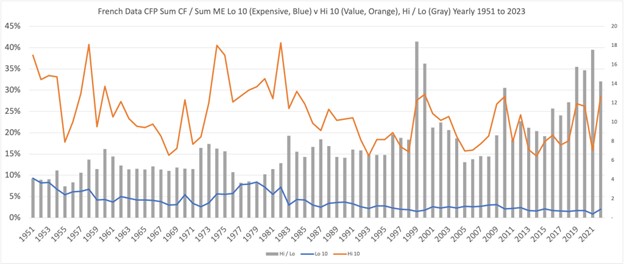

I’d like to direct your attention to the two images at the top, which were brought to my attention by a friend of mine in the industry, Tobias Carlisle. The first chart shows the compound returns of the highest 10% price to cash flow stocks (glamour) and the lowest 10% price to cash flow stocks (value). As you can see, over 72 years, value has outperformed by 5% per annum, and the value portfolio ended almost 20 times bigger than the glamour portfolio. Value investing has simply been the best investing strategy over the long-term. However, since April 2014, the value portfolio in the graph has underperformed by 75%. The spread maxed out at 76% in August of 2020, which was one of the worst years ever for value, closed a bit last year, and then has opened up to near the highs once again this year. The second image shows the yearly cash flow yield of the value portfolio. The two standout timeframes where the cash flow yields were highest, were in 2000 and 2021, simply because the graph doesn’t go beyond 2022, or 2023 would be right up there as well. 2000 was clearly a bubble where the Nasdaq proceeded to drop by 80% over the next 3 years. The current market is dominated by Tech stocks to where the indices are more concentrated than they have been in decades. Valuations in the sector are at rare extremes, meanwhile the primary competition for stocks…. bonds, are offering the highest yields in 20 years. If sentiment were to change, it wouldn’t be a shock to see a massive exodus out of these glamour stocks into bonds and value stocks. I firmly believe that those large glamour stocks have entered into bubble territory, which might end up meaning another lost decade for the indices like we saw from 2000-2010. That decade was bad for the market, but fantastic for value stocks, which posted stellar returns. Our portfolios are as cheap as they have been relative to intrinsic value as I’ve seen, and in comparison, with the overall market, it isn’t even close. We are buying highly profitable and growing companies with dividend yields higher than 5%, and free cash flow yields higher than 13%. These are fantastic metrics that should lead to really strong returns over time. We’ve been taking advantage of the more attractive fixed income environment to capture these higher yields now available. Since 1776, Treasuries haven’t had 3 years of negative returns, but are actually on the verge of that if they finish negative this year. This was fairly predictable given the ridiculously low rates we saw in 2020, but it also offers opportunity to buy securities cheaply. These are times when we can really set ourselves up well for retirement, or whatever other financial goals we have. You have to plant the seeds and let the portfolio grow, but with patience, these can be really fertile times. |