I stumbled on a fantastic article today that is right on target with what we discussed in our previous article from 6/25/20 related to value investing and mean reversion. There is a link below, which I think you’ll enjoy but I’ll cover some of the key aspects. These might be redundant if you read the whole article, but I know from experience that we don’t often click links, so I thought it would be helpful to reference major parts.

Most market participants are short-term oriented, so they end up chasing returns. This activity tends to greatly hurt long-term investment returns. Usually when there is universal pessimism, the best opportunities present themselves. When there is universal optimism, downside surprises are quite common.

“When risks and bad news are known to the market and fear is prevalent, it’s time to buy what’s out of favor, unloved and legitimately creating fear.”

“Asset classes are often declared irretrievably broken after poor recent performance, implying they are unable to provide reasonable forward-looking returns. These proclamations are often now-casts, a common and dangerous financial practice of explaining what’s already happened as if it’s a forecast of the future.”

“In most cases, the performance of a broken asset class is well within its range of historical returns, and outperformance often follows a period of under-performance as mean reversion takes hold.”

“In the five years after an asset class was declared broken, each roared back in a strong, and for many, swift rebound. All except one snapped back within one year, generating returns that ranged from 14% for US stocks to 68% for commodities. The sole dawdler, REITs, rebounded in 18 months, ultimately delivering a cumulative 86% return at the 5-year mark—the weakest performance of the group.”

According to Research Associates, on 49 observations, the 5-year cumulative performance after an asset is declared broken or falls into bottom-decile of returns was 80% on average. 88% of them generated gains and only 12% delivered losses.

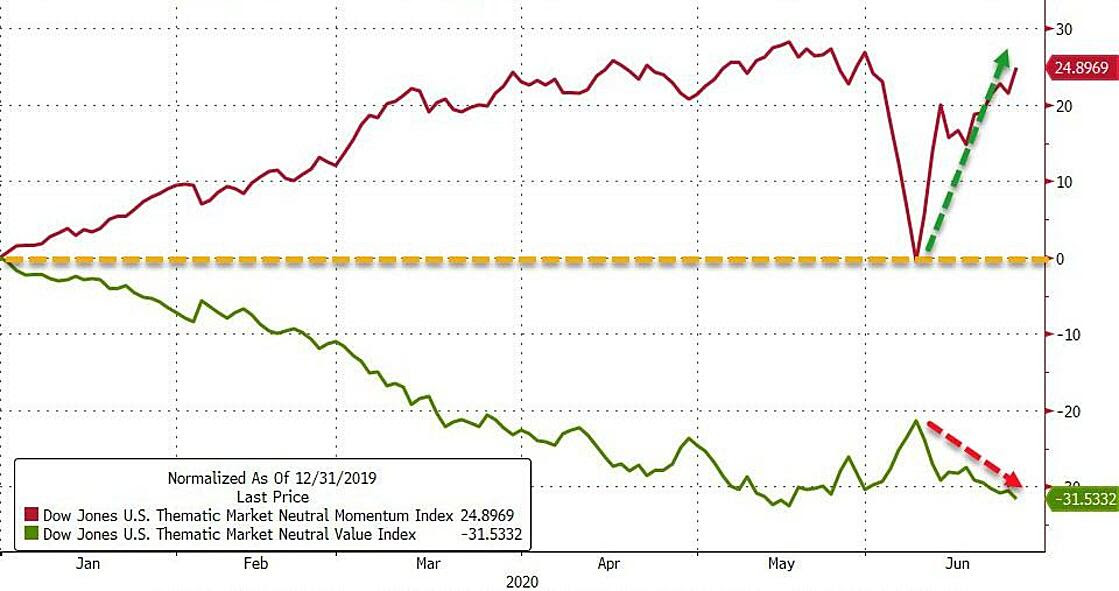

We’ve seen this same phenomenon play out during every major crisis in my career, which spans nearly 20 years, and we are ardent students of history, which is why these studies are so helpful in that they span back many decades. This is as big of a divergence between momentum and value as has ever existed, so the opportunity is massive. We just need to grind through these tough times to get to the other side. I’m adding funds to my accounts whenever I get the opportunity because these are rare opportunities. Here is the link to the full article, which is worth your time.