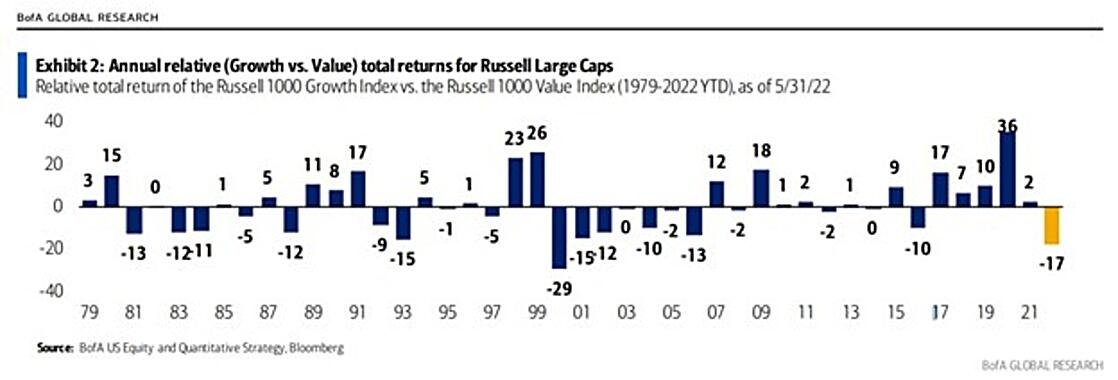

Today there were headlines that one of the premier growth funds, Tiger Global Management is down 52% this year. This has been one of the hottest funds of the last decade, buying the flashiest growth stocks with little regard to valuations. Tiger’s aggressive strategy was richly rewarded over the last few years while value struggled relatively. As you an see from the image at the top of this email, the turn we’ve been talking about towards value outperformance seems to have begun in earnest. The Russell 1000 Value Index is outperforming the Russell 1000 Growth Index by 17% this year. When these cycles turn historically, the change usually persists for at least several years, and of course value has been the best performing strategy in history. This is why it is important to look at performance across a full investment cycle, as it is great to make money, but if you can’t hold on to it profits can erase quite quickly.

I’m very optimistic that factors such as higher interest rates, and compressing valuations, should bode very well for our strategies as value investors. One of the best eras for value was when the Tech Bubble imploded in the early 2000s, leading to 5 of the best years ever, and it is very possible we could be on the precipice of a similar run if we are fortunate. The early 1980s was another great time for value when Volcker broke the back of inflation with higher rates. History might not repeat but it does indeed rhyme, as once again inflation has reared its ugly head, and the Fed is responding with aggressive rate increases.

In bear markets like this, it can be an interesting phenomenon seeing growth stocks turn into value. Recently market participants could only dream of a rosy future, now they can only think in pessimistic terms. The fear is that there is always another downward leg coming, or the stock is likely to be range bound supposedly. By focusing on fundamental analysis and only buying stocks that are trading at large discounts to intrinsic value, we can take advantage of these manic market moods. Stocks such as Google, Facebook, Amazon, and Netflix are just a few examples of formerly glamorous growth stocks that have turned into reasonable value names. Google and Facebook are cheap enough that I really have a tough time seeing how an investor with a 3-5 year horizon would lose money. Below you’ll find my latest research report on Google where I get into more detail.

While many people are understandably concerned about a potential recession, one must remember that the market is a discounting machine. It’s already pricing that into stocks and, generally, the market recovers far ahead of the actual economy. As Warren Buffett says, “you pay a rich price for a cheery consensus.” Well few people are super cheery right now. If we get a peace deal between Russia and Ukraine, we could see a substantial recovery in the equity markets. Unfortunately, that doesn’t seem likely with the continued escalations between the parties, but it would materially improve the economic atmosphere. Shanghai just lifted its dystopian lockdown and consumer spending is still strong, which is the majority of the economy. If we get anything but the worse outcomes (such as a nuclear detonation), I think we have the potential for great results over the next two to three years between our long stock positions and our options, which we are selling into this massive volatility. If value goes on a big run, that would be additional wind behind our sails. I hope you enjoy the Google research report along with my most recent Bank of America write-up.