There was a great article on Bloomberg today discussing the shift towards value investing and the opportunity available that you can find here. The article might require a subscription so I’ll highlight some of the key points.

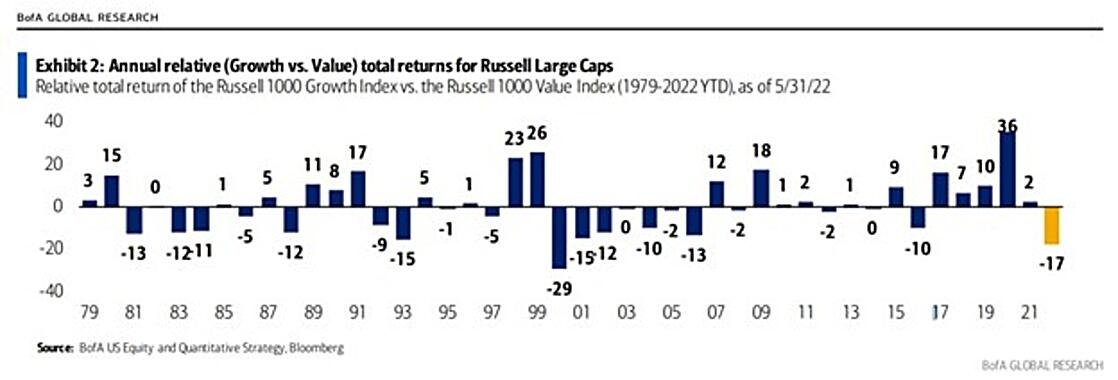

“After languishing behind growth for most the past decade-plus, value investing has come back with a vengeance. The S&P Pure Value Index, which tracks companies with low valuations based on ratios of their share price to their book value, earnings, and revenue. Since the middle of November, the index has returned close to 8% with dividends. Over the same period, its sister index, the S&P Pure Growth has lost investors 25%.”

Pure value has a higher stake in financials and energy, with less exposure to information technology, which was the most expensive sector. Many market participants attribute the shift to higher interest rates, as lower rates promotes risk-taking, as the opportunity cost of forgoing current earnings and cash flows for more growth is less costly in a low-rate environment. I definitely believe there is truth to this, as we are already seeing glamourous growth stocks such as Carvana, now struggling to find access to capital without paying exorbitant rates, as lenders also become more concerned with actual profits, instead of simply relying on extremely optimistic growth forecasts.

In the article, Rob Arnott points out that most of the outperformance Growth saw was tied to valuations expanding, while Value multiples either contracted or stayed the same. It’s normal for growth stocks to be about five times as expensive as value based on book value, but even after the reversal over the last 6 months, growth is still 8-9 times more expensive, so there is still plenty of room to run for value.

As we have been discussing in recent newsletters, at TTCM we are taking advantage of growth stocks getting crushed and turning into value stocks in many cases such as with Alphabet, Meta, and even Amazon to some extent. We are happy to own virtually any industry or sector, but we always want to buy at discounts to our estimates of intrinsic value. This allows us a level of protection that many have found themselves not having as they have gotten hit hard by this bear market.

We’ve got a really good opportunity to take advantage of this pessimistic environment and add high quality companies at prices where we should expect double-digit per annum returns, which I believe will exceed the returns achieved from the indices at current levels. This combined with our ability to take advantage of robust volatility by selling options at extremely high premiums provides us a great opportunity to protect and grow our hard-earned capital, even if the overall market remains quite challenging. Here is a recent research report we wrote on Restoration Hardware (RH). This is a new small position that we have been investing in with options, by selling puts at $200 or less, while the stock trades above $300, already down 60% from its 52-week high of $744.56. If we get exercised, we’d have 50-100% of upside on owning the stock, or we should achieve very robust options returns if the stock stays above $200. Warren Buffett’s Berkshire Hathaway is the largest shareholder owning over 8% of the company. There are a number of great options positions like this embedded in our portfolios’ and we just need to harvest them as they expire over the next year to realize the full potential.