Dear Investors,

Warren Buffett says, “The less prudence with which others conduct their affairs, the greater the prudence with which we must conduct our own affairs.”

As stock markets across the globe continue to hit record highs, it is important to take a measured look at the environment around us. Volatility has been exceptionally low all year, which is a reflection of a lack of concern for a big market fall. Junk bond spreads over Treasuries are some of the lowest that we have seen. Most stocks have gone up far more than their earnings have risen, extending valuations to worrisome levels. As a result and based on the Schiller inflation-adjusted index, stocks are more expensive than they have been in history aside from the tech bubble in 2000.

We contrast these seemingly worrisome indicators with a strengthening global economy and the prospect for lower tax rates. While higher global growth is extremely positive, one secondary impact of it could be higher inflation. This would likely lead to higher interest rates, which would put enormous pressure on bonds and many stocks. While it is important to not overrate geopolitical drama, we would be negligent to not mention that the specter of conflict with a nuclear-enable North Korea remains in the periphery.

In this environment, we at T&T Capital Management feel that it is extremely important to stay disciplined. Being disciplined means the following:

- We will only invest in securities in where we feel there is a considerable margin of safety. This sets the stage for attractive returns and provides protection in adverse conditions.

- From a portfolio management standpoint, we will employ strategies such as cash-secured puts and covered calls, which provide additional protection and income. While these strategies might reduce upside potential in extremely buoyant markets, they do allow us the opportunity to buy stocks at cheaper prices, and generate additional cash flows. Given that we aren’t exceptionally bullish on the overall market, these strategies over the long-term should provide us with some significant long-term benefits as they have in the past.

- We will focus on our best risk-adjusted return opportunities, meaning more focused portfolios. One major reason why most funds underperform the indices is because they basically try to follow the indices, and then add their fee on top. This provides no value whatsoever. I never can understand why it would make logical sense to invest the same amount of money in your 20th best idea, as you do in your top idea. I do know why fund managers do that though, and it is because they are afraid of looking stupid by doing something different and getting fired.

The major reason why so many market participants perform poorly over the long-term is a focus on short-term performance. Most people might intuitively understand that paying negative interest rates for sovereign European debt is idiotic, the buyer of the debt may only be concerned if those bonds go up over the next quarter. The same short-term logic is what is really motivating prices of most securities, which are clearly past the point of offering any real margin of safety. Fortunately, markets are mean reverting over the long-term. What looks smart one quarter, looks moronic the next. Value investing has stood the test of time because it makes intrinsic sense.

- Stocks are fractional shares of a business.

- Every business or stock has an intrinsic value.

- By buying the business or stock at a discount to intrinsic value, one can feel confident in an adequate margin of safety and attractive return potential.

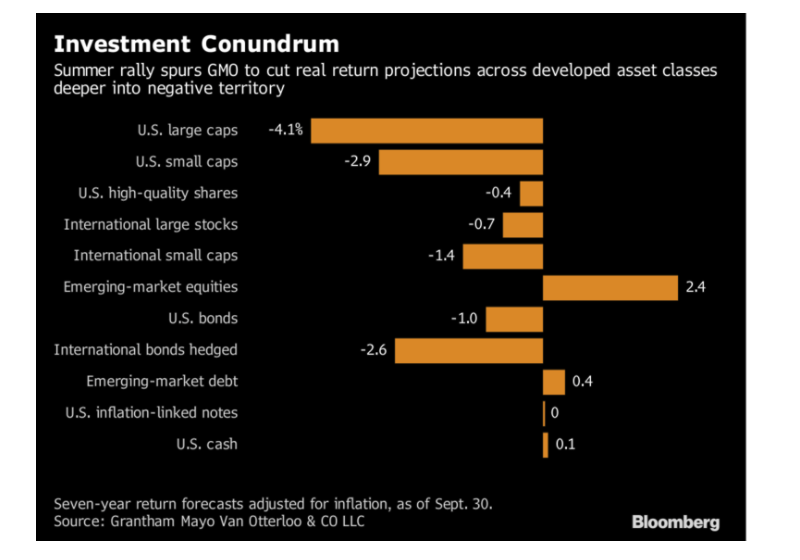

Below are some forecasts for various asset classes for the next seven years on the first one, and year in the second. A forecast is simply that and shouldn’t be relied on in most cases, but GMO is a really solid firm that takes a quantitative look into the future based on valuation and growth metrics. It really is simple math, that tells us that most stocks and bonds simply must return far less over the next 5-7 years, unless we are going to be in a bubble like we have never seen. The last link is to an excellent interview with Howard Marks, where he discusses current market conditions and how it is essential to maintain discipline throughout market cycles.

Global Investors Brace for a Cruel New World of Feeble Returns

Howard Marks – Most Great Investors Stick To An Approach Through Thick And Thin

Sincerely,

Tim Travis