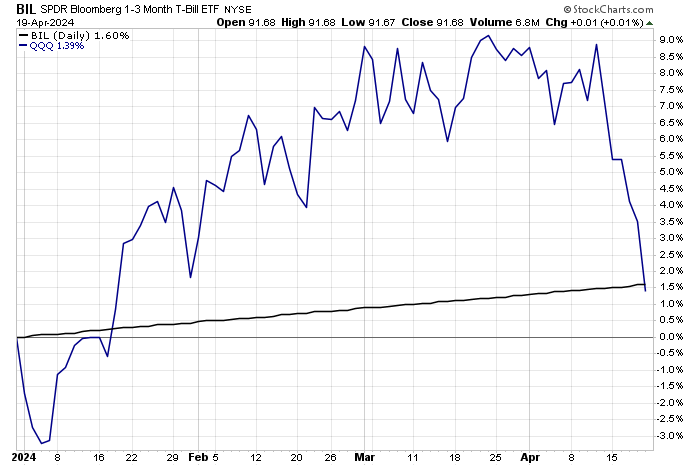

Higher than expected inflation and geopolitical turmoil have begun to roil the equity markets of late, wiping out $1.3 trillion in value last week alone. This past week, the S&P 500 declined by 3%, recording its 3rd consecutive week of declines. The Nasdaq declined by 5.3%, which was its worst week since October 2022. Many of the Magnificent 7 were down greater than 10%, including Nvidia. As you can see from the image at the top of this email, T-bills are now outperforming the vaunted QQQ’s YTD, despite the torrid start to the year that the Nasdaq had. Remember the story of the Tortoise and the Hare? One of the big themes that we have been writing about in this newsletter is that the speculative frenzy that has pervaded the stock market, seems to have gone too far. It is so easy to see a great first quarter and think you don’t want to miss it, so you just keep adding more risk. Ultimately, that is what blows you up. As risk managers, we want to take a business approach to investing. This means only allocating money where we have the expectation of profit base on fundamental analysis, not simply gambling.

In the current market environment, we can get yields on investment grade bonds varying from 6.3-7.8%. In the high-yield space, we can get between 7-9.5% on what we perceive to be pretty attractive investments. These are pretty attractive returns in the context that one is taking far less equity market risk than the vast majority of investors. If we do get a recession and rates go down, that would likely push returns comfortably into the double digits. The recent increase in interest rates has provided another opportunity to load up on some of the highest quality commercial real estate assets in the world, paying dividends between 5.5-8%, with upside between 50-100% over the next 3-5 years. Once again, I’m excluding Office, which is just a bit too speculative given the changing dynamics. I like these risk/rewards quite a bit, and we are enhancing the yields further by incorporating covered calls when appropriate, pushing the cash yields to 10% or more in many cases. I don’t think we need to be super aggressive on equity risks to get equity-like returns, and I think this has positioned us to dramatically outperform if we do indeed get a bear market sooner than later.

Persistent inflation pressure makes it more likely that the Fed cannot begin to cut interest rates, which is what much of the rally from October lows has been based upon. Our position at TTCM, has been that for inflationary pressures to truly subside, you’d likely need economic weakness, probably reflected by higher unemployment numbers. Look at the housing market. Homebuilder stocks look like Nvidia with the appreciation they have achieved. Despite soaring mortgage costs, residential housing prices really haven’t pulled back that materially, except in a few overbuilt markets. Commercial real estate values have declined predictably with higher rates, but residential has been far less bothered. To me this phenomenon is unlikely to persist. Either residential prices should correct a bit, or interest rates seem to need to decline to justify current prices.

In terms of geopolitics, I don’t remember a year where we didn’t have major issues, but with that said, this year is even worse than usual. You have two major wars in Ukraine and the Middle East. Beyond that, you have many of the major powers participating via proxy, providing money, materials, and manpower to further their interests. Calls for peace don’t seem too popular among the political class, so a resolution in the near term doesn’t seem too likely.

These concerns don’t mean you shouldn’t be investing, as often the best time to invest is when there are a lot of perceived risks. What is interesting about this market though, is that equities reflect incredible optimism in spite of the considerable risks and high valuations. Conversely, high-yielding bonds and real estate, which pay predictable interest payments and dividends, with upside appreciation potential upon declining rates, are available at truly attractive levels.

Given these factors, I’d rather be positioned to dramatically outperform in a bear market, or a flat to slightly positive market. If the stock market tears upwards and continues perpetuating the bubble, I’d expect to underperform, but I’d be okay with the knowledge that bubbles ultimately do pop and you don’t want to be there when that happens. We held up quite well in this nasty week, and you’ve likely noticed that we tend to have a lot less volatility on some of those big down days. The security of our strategy would be much more magnified if we were to see a bigger downturn. Month in and month out, we are collecting our interest payments, dividends, and option premiums. We will see what happens, but I can tell you that we are finding great opportunities, by taking a lot less risk than the vast majority of investors, and I think not following the sheep is the correct risk management strategy! I hope that you all have a fabulous weekend and please let us know if you need anything at all.

Here is a link to all of our most recent radio shows where we have been covering a wide variety of financial planning topics each week: Radio Shows

If you enjoy our newsletter, please feel free to forward to friends, as that is how we grow.

Thank you very much and please let us know if you need anything at all!