Markets continue to exhibit higher volatility due to economic data that indicates that higher for longer Federal Reserve interest rate policies are more likely. At TTCM, we view predicting macroeconomic data as being a rather pyrrhic enterprise, as success rates for even supposed experts, are far less than 50%. By focusing on individual securities and only buying them when they are deeply undervalued, we can play a game we understand and can succeed in. This isn’t unlike the batting approach taken by legendary Hall of Famer Ted Williams, which was described as the Science of Hitting. Williams would segment various hitting zones and track his success rates. Instead of chasing balls that were in his weaker areas, he would stay disciplined and wait for pitches that he had a higher probability of being right on. This is the only sensible approach to investing in our estimation.

By focusing on undervalued securities, we can be flexible in the types of securities we are buying. For years we avoided bonds, as the zero interest rate policies created an epic bubble that has devastated portfolios across the globe. Well after the carnage there is now opportunity, and here we are buying bonds at high yields that offer considerable protection, cash flow, and upside potential when interest rates do head lower once again, whenever that may be. As we discussed in our previous newsletter, we have a very high hurdle rate to invest in equities, as we want the combination of earnings yields and future growth rates to make the investment a vastly superior option than what we can get buying some of these interesting bonds. We use the same philosophy with the cash-secured puts and covered calls, we are targeting very robust returns and an extremely strong margin of safety.

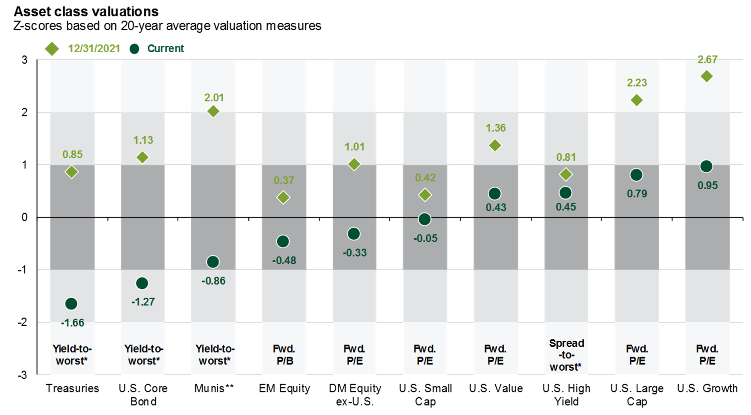

A lot of market participants are thinking we are heading right into a roaring bull market like after 2012, and while that would be wonderful if it proves to be the case, I think we are far more likely to be in a range bound and challenging market. The image at the top of this email shows that U.S. growth stocks are the most expensive area of the market relative to historical averages, while smaller cap stocks, fixed income, and value offer far better opportunities. Mean reversion is a powerful phenomenon and I believe it should continue to work in our favor.