Dear Investors,

Today we are launching our new blog www.ttvaluetalk.com. The point of the blog is to educate and inform investors on beneficial investment and financial strategies that we employ at T&T Capital Management. While we have done a newsletter for years, our content has been kind of hidden within the website, so we felt it was important to create an individual site dedicated to our content, which we hope that you will find enjoyable and helpful. Please don’t hesitate to invite friends and family to join as I 100% believe that those that read it will have a better chance at creating a stronger financial future, which is our primary goal.

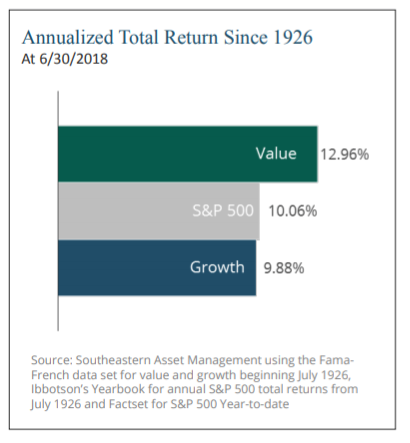

I’d like to start with why we believe so much in value investing. Below is a table produced by Southeastern Asset Management that clearly shows that value has outperformed the S&P 500 by nearly 3% per annum since 1926. $100,000 compounded by 13% per annum over a 40-year period ends up with a future value of $13,278,155. At a 10% return over 40 years, the future value is $4,525,925, making for a staggering $8.7MM, or 66% differential in growth.

Now there is no guarantee that future returns will be as good as the past for the stock market, but over time businesses and economies do tend to grow, making equities the preferred way to invest over the long-term. If you look at the most successful long-term investors that have multi-decade track records such as Warren Buffett, Seth Klarman, etc., nearly all of them utilize value investing as their primary investment philosophy. That isn’t to say that other strategies can’t be successful and even outperform over a reasonable period of time such as a decade, but by utilizing the value investing method, you are enhancing your odds of long-term success. Of course, the only way that you keep the odds in your favor is by sticking with it and maintaining your discipline, which is one of the most difficult things to do for market participants, but that is consistent with any investment strategy.

I was fortunate to have worked at a variety of different financial firms in my early 20s. This was helpful mostly because I learned what not to do. I saw Vanguard and index funds after the tech bust, and how those that had been piling into indices were negatively impacted. I saw that Scottrade at that time offered no investment advice, leaving many of its clients chasing whatever the hot speculative stock at that time was. I also saw how brokers at full-service firms would focus 100% on commissions with very little regard to their respective clients’ best interests. Even more beneficial to me was that I also found the time to read extensively on a variety of different topics, which has and continues to shape my investment and personal philosophies. Market participants must understand the mantra of Wall Street; they will sell you anything that they can make money on. Usually that sales pitch is surrounded by a storyline, where salesmen that probably aren’t too steeped in the actual investment analysis can quickly summarize an idea to their clients to get them in the trade/investment. While I used Wall Street as a reference, this is a broad group that includes real estate, insurance, commodities, and yes even investment advisor professionals like myself. The products and pitches change but the psychology behind it rarely does. Salesmen love selling what has worked recently, whatever that is.

In the 1990’s, this meant technology. Storylines such as how many people would view a certain website, overtook normal financial fundamentals such as earnings and cash flows, to rationalize why an analyst would recommend a high-priced stock. The mid-2000s saw a full-fledged national housing bubble erupt, setting the stage for the biggest recession since the Great Depression. The storyline was that housing prices had not dropped on a national level since WW2, so you had to buy as soon as possible before prices went up further. After the ensuing Financial Crisis, many market participants were disillusioned with the stock market. Salesmen once again took advantage of that sentiment by pitching high-priced and low-returning annuities and gold investments. These investments have dramatically underperformed equities, and this was not hard to predict if you were able to detach yourself from emotion and instead focus on fundamental principles, such as valuations.

Let’s fast forward to today’s environment. We are in year-9 and a half of a bull market. By most metrics, stock valuations are the most expensive they have been in history, except for during the Tech Bubble, which of course ended disastrously with stocks losing about 75%. Unsurprisingly though, most salesmen or “Wall St.” are pitching mostly index funds, which is evident by fund flows. Once again, this is a case of a good idea with historical weight, given that most active managers underperform, but it is extrapolated way too far because it is easy to sell. Firstly, most “active” funds are closet index funds. If you have over 100 stocks in your fund, you are statistically nearly identical to the index. Then if you add on fees, you are almost guaranteed to underperform. Even worse, most advisors put their clients in a wide variety of funds, further over-diversifying them, making the math that much more challenging. If that is how you want your money invested, you should expect to underperform, and an index is a fine option.

However, if you focus on value and concentrate your investments on your best 15-30 ideas, your chances of outperforming over the long-term become far more evident. Today’s environment certainly shares some parallels with 2000 as far as valuations go, and let’s not forget that value investors had some of their best years following the tech bust, despite the market plummeting. It took over a decade for most investors in index funds to recover their losses from 2000, and it took quite a few years after 2008 to recover as well. Advocating to go 100% long stocks, which is what the S&P 500 is, while paying no respect to valuations is not intelligent investing. Sure, if you invest in that index and leave it for 40 years, you will probably do well as most long-term investors do, especially if you keep saving and dollar-cost averaging.

I’d argue, and the nearly 100-year track record of value investing would say, that you would be far better making valuations the central determinant behind your investing decisions. Clearly, patience and continuously saving are just as vital as with an index, but I believe that this aggressive pitch towards indexing will likely prove disastrous over the next 5-10 years. Don’t forget that this sales pitch wasn’t nearly as pervasive until the last 5-years or so, when we were already 4-years into the bull market. These genius advocates of index investing weren’t nearly as vehement in their philosophies when things were actually cheap, yet now they have reformed themselves with the hindsight of a nearly decade-long bull market. We’ll see how their philosophies change when faced with real stress and the reality of market participants’ psychological behavior, which is as old as civilization.

Up until about 2013, the common rhetoric was buy and hold is dead. In fact, I just watched an interview on CNBC where the portfolio manager of the Illinois Pension plan explained that he shifted 66% of its assets to passive management three years ago. Probably not a bad decision if they stick with it for 40 years, but I doubt that they will and in doing this they are likely exposing their constituents to considerable risks of low-returns given the valuations in both stocks and bonds.

Products like market-neutral funds and managed futures proliferated, which have of course been terrible performers relative to stocks over the last 5-years. If you are buying an index at current levels, you must be prepared for a 30-50% haircut. If this type of drop in your account value would cause you to change your behavior, then you are now actively managing your money and returns will likely be far worse because you’d be selling near the lows most likely, and probably wouldn’t get in until markets have mostly recovered.

Value investing does not prevent you from taking huge drops either but focusing on fundamentals generally leads to fewer losses and stronger recoveries, which is why in the long-run returns have been better. Even the great Berkshire Hathaway has had several periods where it has dropped by 50% or more, but obviously those dips were phenomenal buying opportunities.

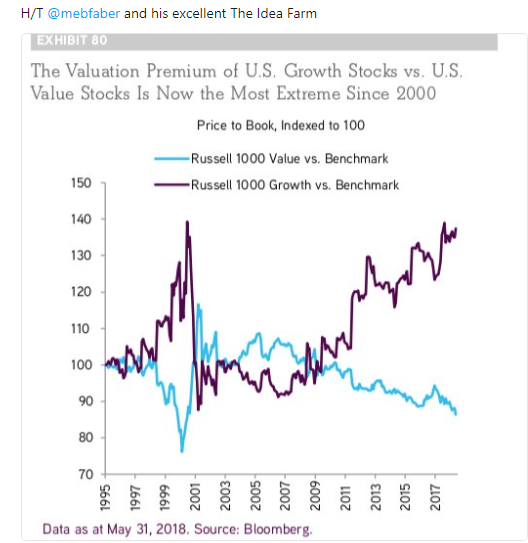

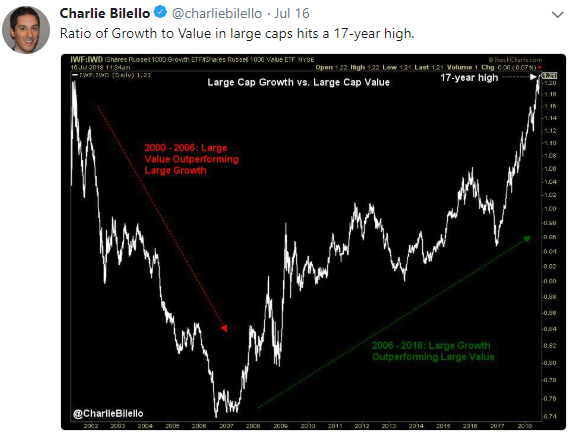

For instance, at T&T Capital Management, we start with value investing as the fulcrum of our philosophy, but then add strategies such as selling cash-secured puts on value stocks, distressed debt, and covered calls, to reduce risk and enhance income. These strategies might cause us to underperform in a year like 2017 when markets did nothing but rally, but over time they have allowed us to outperform the S&P by a slim margin in literally the worst environment for value investors ever. Below are two graphs that show that the valuation premium between growth and value is the highest it has been since at least 2000, which is really the only parallel.

In addition to compound interest, the most powerful dynamic in markets is mean reversion. After 2000, the “old world” stocks rallied dramatically even while the indices plunged. This is why value investors outperformed after underperforming during the Tech Bubble, because these stocks traded at undemanding multiples of cash flows and intrinsic value.

Many of the indices such as the S&P 500 are dominated by stocks such as Amazon, Netflix, Facebook, and Google, which have really been the pillars of growth stocks’ outperformance over the last decade relative to value. If we see mean reversion, we likely would be in a phenomenal environment for value investors, while the overall market and growth stocks might have some serious issues. I’d be a fool to tell you when exactly that is likely to occur, but the odds and history would imply that this should happen sooner than later.

In summary, that is the bet we are making, which really is no different than how we always have managed money. Our focus is always on maximizing risk-adjusted returns over the long-term, with risk defined as permanent losses of capital. Of course, we adjust our strategies based on clients’ short-term needs when necessary, but for the most part our eyes are laser-focused on these priorities. Skin in the game is essentially what motivates us and proves our conviction. 100% of mine and my family’s money is invested in the same strategies as we do for clients, so we eat our own cooking through the good and the bad.

Investing without respect to valuation is not intelligent behavior. Maybe people made a fortune on Bitcoin if they got in early but soon the bubble burst. How many people bought in the end of 2017 and held after the 60% decline? Maybe those that sold were smart to limit losses or maybe they were like the ones that sold Amazon after its crash in the early 2000s, only to miss the monstrous rally that has occurred since. Most investors can’t identify the next Amazon, but if you stack the odds in your favor, over the long-term you really can outperform.

This is probably a good place to leave it for now, but as always if you have any questions or if I can help you with anything, please don’t hesitate to contact me directly at 805-886-8140!

Sincerely,

Tim Travis