Dear Investors,

For those of you that have been with us for a long time, you know that one of the key elements of our strategy is to load up on positions when prices make no sense, offering huge upside and a large margin of safety. In today’s expensive overall market, there have been a few good opportunities, particularly for income-generating stocks, but not the type of situation where we feel we could really knock it out of the park since many of our large financial stocks have appreciated so much. In the wake of Hurricane Maria, this has changed and we have the most attractive investment opportunity since the Brexit selloff last year.

Assured Guaranty (AGO) has sold off materially over the last week to just over $37.50. To put that in perspective, the 52-week high on the stock was $45.72 and the 52-week low was $26.37. At T&T, we have been investing in this company for over 8 years now and have made many millions of dollars in it for clients and for ourselves. The investments have been successful because the company is poorly understood by the overall market due to an obscure industry, and management has done an exceptional job at increasing intrinsic value per share each year. While the chart below shows how successful the investment has been, it should not be underappreciated how there have been many periods where the stock has declined by 15-25%, throughout the general uptrend. Every single one of these selloffs has been a great buying opportunity!

The primary reasons for this recent selloff are a combination of the following:

- Hurricane Maria devastated Puerto Rico and this could delay the eventual restructuring of the island’s debts, all of which are in default. The Supervisory Board that has been in charge of the restructuring until now has been incredibly negative for creditors, making a variety of completely illegal decisions to garner negotiating leverage against creditors. Ultimately, the situation will likely be worked out via court where I expect recoveries will be much better than what is currently being discussed by the media that is not that well-versed in bankruptcy procedures for municipalities, although this is a very unique scenario. We all want the best for the citizens of Puerto Rico, which have suffered through decades of terrible governance and now are desperately trying to recover from the worst hurricane to hit the island in at least 100 years. Having access to capital is imperative to accomplish these goals.

- Hartford, Connecticut is likely going to declare chapter 9 bankruptcy. This is a relatively small exposure but it is another negative on top of Puerto Rico.

Puerto Rico’s ultimate resolution is very uncertain and realistically is impossible to accurately forecast. The good thing is that the risk itself is very quantifiable and due to the company’s impeccable balance sheet, the company is in excellent shape. Despite Puerto Rico, AGO has never been in a stronger financial position. In addition, new business production is starting to grow rapidly and should be very profitable.

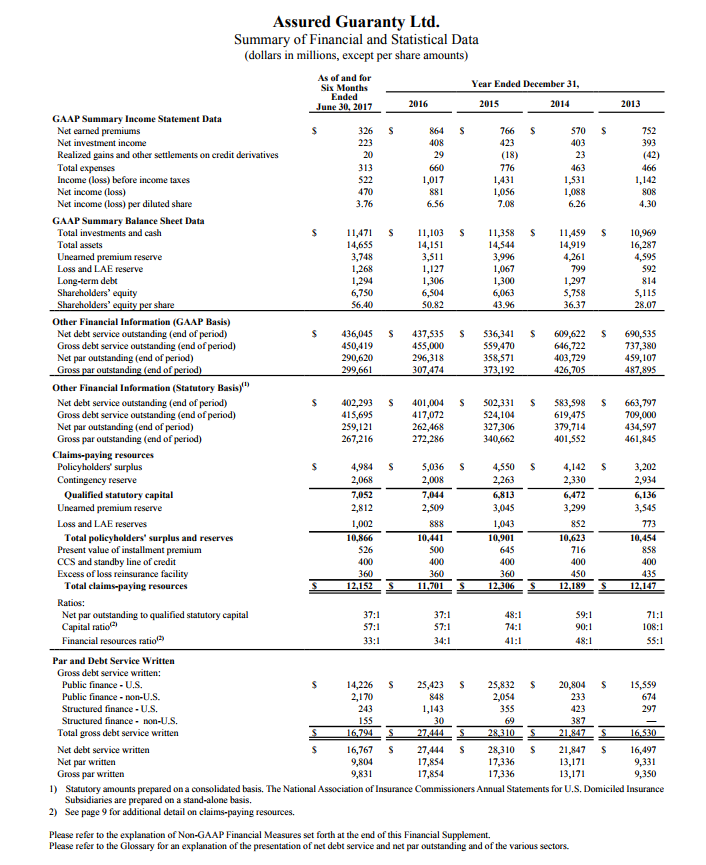

To evaluate Assured Guaranty, you can start from their book value of $56.40 and their adjusted book value of $73.48. The difference between the two numbers is that adjusted book value incorporates the net present value of the company’s in-force premiums and revenues net of expected losses. The company’s biggest liability is its unearned premium reserve of $3.748 billion. This is the best possible liability as it has already be collected and AGO is able to invest the money for decades, earnings interest income. Ultimately, the unearned premium reserve minus any expected losses, translates to earned premium revenues. In a normal environment where AGO is writing new business (as it is currently), AGO should be valued in between book and adjusted book value.

As you can see from the table above, book value per share has nearly doubled over the last three and half years! This growth has been the result of retained earnings, stock buybacks done at large discounts to book value, and accretive acquisitions of its distressed competitors. Because of the record-low interest rate environment that has existed over the last 8 years, new business production has been far lower than historical averages. This has meant that Assured Guaranty’s in-force insurance book has declined more rapidly than production, which has resulted in a deleveraging of the insured portfolio. At the end of 2013, AGO’s net par outstanding to qualified statutory capital ratio was 71:1, down considerably from peak levels, which were well over 100/1. As of the end of the 2nd quarter of 2017, that ratio has nearly been halved and stood at 37:1. These improved capital ratios are what create excess capital, which AGO has used to buy back stock at attractive prices. Keep in mind that these ratios have improved so dramatically despite the company buying back about 40% of its stock and making several acquisitions over the last 4 years. Puerto Rico has been a problem for the last 3 years and has driven the company to reserve between $1 billion to $1.2 billion at least to cover losses for its $5 billion of exposure. These are losses in excess of the premiums collected when the bonds were first insured, which still sits in AGO’s unearned premium reserve. Many of the bonds insured by AGO are the strongest credits with revenues that should be dedicated specifically for paying interest and principal payments, or GO bonds that should come before even government salaries according to the constitution.

Assured Guaranty has a long history of being overly conservative on its reserve estimates, as proven through the Financial Crisis. Let’s assume for argument’s sake that AGO has under-reserved by a whopping $1.5 billion. Using a 30% tax rate, this would result in a loss of $1.05 billion. AGO had 119.7MM shares outstanding as of the end of the 2nd quarter and I’d expect them to buy back about $100MM of stock per quarter over the next few years. Using the 119.7MM figure, the loss per share would be about $8.78. Average yearly payments on 100% of its Puerto Rico exposures is less than the annual investment income from the $12 billion dollar investment portfolio, which is greater than $400MM. This is important to note because there will not be a liquidity crisis whatsoever and many of these bonds extend out 20 or 30 years so the future value of payments is far lower than the nominal number. Assuming no other profits or stock buybacks, adjusted book value per share would still be around $64 and book value would be around $46. AGO has already earned $3.76 YTD over the first 2 quarters, despite steadily increasing reserves for Puerto Rico. The company should remain profitable over the next 2 quarters and through buying back stock at a discount, book value will continue to grow. This recent selloff is fantastic for the long-term intrinsic value of the stock.

As far as how we trade the stock, we have always employed a variety of buying stock outright, selling puts, and selling covered calls. There have been many times where the options have expired worthless allowing us to capture the full profit, enhancing our income, and there have been other times where we have been exercised. All of this has served to reduce our cost basis on the stock. I believe the stock will ultimately go higher than $55 but the timing of that is uncertain. Now that volatility is increasing, we are able to sell long-term puts on the stock at mid-teen annualized rates of return. To be clear, we feel that the stock has very low risks of permanent losses of capital but selling puts is an even safer way to profit. Given our belief that the market itself might not even be positive over the next couple of years, the potential to make mid-teen returns over the next few years is too good to pass up. Earlier this year, we were able to take profits on millions of dollars of AGO puts and stock as the stock appreciated. Most of our other positions have been performing really well, so we’ve been able to lock in additional profits on them. This is enabling us to get more heavily involved once again with AGO for what we believe to be one of the most attractive risk-adjusted return opportunities that we can find. For those of you that have excess money outside of your TDA accounts with us, please don’t hesitate to give me a call to discuss your options and whether increasing your allocation would be appropriate. I can tell you that I am both adding funds to my accounts, and am massively adding to my own personal positions in the stock. With that said, there is no guarantee on anything and especially over the short-term, the stock could continue to drop. This is a big reason why we use puts in the first place.

As always, keep your focus on the long-term and the fundamentals, and don’t stress about short-term fluctuations, which tell you nothing of importance. Instead let’s use these hiccups as opportunities to create and grow wealth. Thank you very much and as always feel free to call me anytime directly at 805-886-8140!