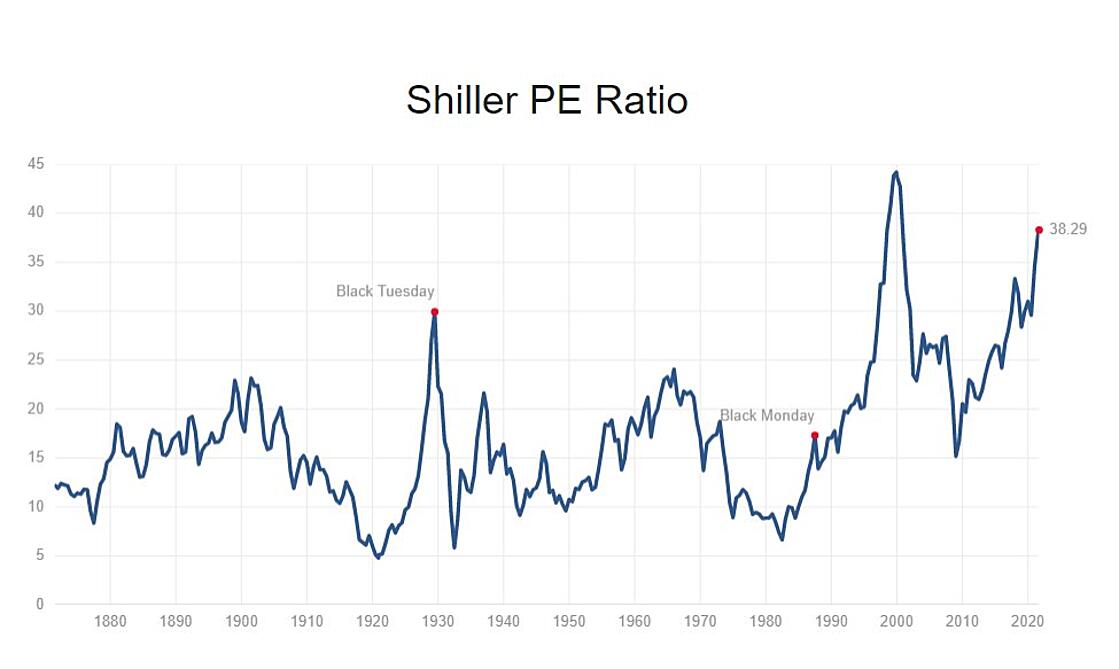

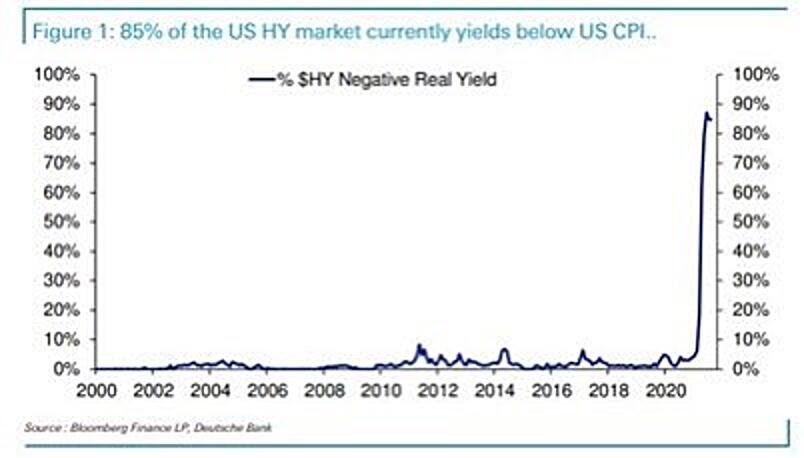

In our last newsletter written on Friday, we wrote about just how much risk market participants are having to take to target a 7.5% return, mostly due to how low yields are on bonds. The bailout has been that equity markets have performed exceptionally well, but of course now we are starting at valuations that are some of the highest in history. It is in an environment such as this that the flexibility and customization of using stock options, can add a really exciting and profitable element to our investments.

Citigroup stock is trading around $71.50 as I’m writing this. The tangible book value per share of the stock as of the end of the 3rd quarter of 2020 is $79.07. This is the closest proxy for liquidation value. The bank has already posted $8.65 per share in net income YTD through three quarters. Some of these earnings are reserve releases as credit has been way better than had been anticipated during last year’s recession. Here is our latest research report on the stock for more info: Tim’s C Research Report.

Let’s say we want to target roughly 7.5% per annum returns. We could sell a $62.50 put on C expiring in January of 2023, or 459 days out, for $5.30.

If the stock trades above $62.50 at expiration, you will make $530, on a maximum risk of $5,720 ($6,250-$530). This is good for a 9.26% return, or about 7.4% annualized. Your breakeven price for C would be $57.20 per share. This means that Citigroup would have to drop by about 20% for you to actually lose any money, assuming we hold the options till expiration. Citigroup is already trading at a discount to tangible book value per share and will almost certainly grow that metric by between 5-10% over the next year via retained earnings and accretive stock buybacks. The company is returning nearly all of its earnings to shareholders via dividends and stock buybacks, as the bank has excess capital.

While we believe Citigroup is still an undervalued stock and do own it outright, we feel that this type of attractive risk/reward from using options makes a great deal of sense. This type of strategy provides ample protection upon a major market downturn, as long as we hold the options till expiration. Short-term swings in price can have major impacts on volatility pricing, so to see the full protection we need time and volatility to go to zero, which happens upon expiration. Hopefully this example sheds a little light on the attractive opportunities and strategies that we are able to use, and why we feel they are very advantageous in a world in where even junk bonds are yielding less than 5% in many cases.