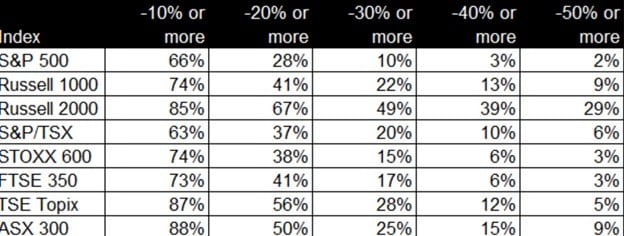

Stock market volatility has continued with a vengeance throughout January as inflationary concerns, and the coinciding likely interest rate increases to combat it, are front and center on investors’ minds. In addition, while the economy is still reasonably strong, how durable would it be in a higher rate environment? Throw into that mix geopolitical uncertainty in relation to the Ukraine/Russia spat, and you have yourself a nasty little market. 66% of the S&P 500 is down 10% or more, 28% is down 20%. In the small cap Russell 2000, 85% of companies are down 10%, 41% are down 20%, and 22% are down 30% or more.

While these story lines play their part in the volatility, the root of the problem is that we’ve been in a nearly everything bubble for several years. As you can see from the image at the top of the email, the most expensive quartile of stocks saw their Price to Earnings ratios expand from 22.8 at the end of 2016, to 30.7 at the end of 2021. Meanwhile the cheapest quartile best defined as value stocks actually saw their valuations decline. Business performance was good for all three groups, but it was the mean divergence, which created the massive spread in valuations. Fortunately, value stocks have held up much better than the overall market and especially growth stocks through January, and we are very optimistic on the future, as the stocks trade at meaningful discounts to their intrinsic value, despite excellent business performance. Dividend yields are very high and we’ve been very aggressive selling covered calls to double or triple those dividends in many cases.

At T&T Capital Management, we have taken a very disciplined and prudent approach to investing. The volatility index (VIX) has exploded higher over the last few weeks. This has enabled us to sell cash-secured puts and covered calls at very large premiums, even when these options are far away from the market. This creates a situation where we either should earn a very good return with the options expiring, or we’ll end up buying or selling the stocks at prices that we feel fantastic about. Often the options we are selling are 25-60% below current market prices, despite those stocks having already dropped substantially. We will reap the benefits of this strategy over the next year as time value and volatility levels drop. If the market gets a lot worse, we would have the potential for many years of growth getting exercised on these options at the prices we are talking about. This would be distressed investing 101 and is often where the most lucrative long-term returns are found.

While there are definitely some very attractive stocks at current levels, the risk/reward with the options is what I believe to be most unique. I don’t think the market is close to cheap even after this downturn, however the economy is still quite good. Omicron should start declining and the supply chain should improve. This will enable businesses to continue to operate well and make money. This is much more of an old fashioned stock market bubble deflating a bit and it is a good opportunity for value investing to really shine over these next few years.

Market participants have gotten rewarded for the last decade for buying every dip. Certainly buying stocks as they get cheaper in intelligent, but it is more important to buy at discounts to intrinsic value. A stock that has declined 50%, could easily decline by another 50%, if it was dramatically overpriced to begin with and unfortunately many people are learning this lesson. In this type of market, it is imperative to know what you own and why you own it. That analysis is what gives one the confidence to hold, buy more, or sell if need, during times of turmoil. Everyone seemingly has a high risk tolerance in rising markets, but that can change quickly when you get into a major correction, or if this turns into a full-fledged bear market. Our ability to utilize options as a tool to generate income, reduce risk, and to manufacture dramatically cheaper entry prices into stocks is a major advantage in these market conditions, as we don’t have to be perfect on our timing.