Value investing is all about buying companies at a deep discount to intrinsic value. Often these companies are dealing with short-term issues such as a cyclical downturn. Today we closed out one of our larger positions, which was in the agricultural equipment manufacturer AGCO. We bought the stock mostly in the low to mid $40’s and closed out today in the mid to high $50’s. The stock is up over 25% year to date. Much of the optimism is due to the expectation of an El Nino weather system that is expected to cause an increase in agricultural prices. The stock is very close to our target price of $60 and we feel that with the volatility that is now presenting itself, we can find better risk-adjusted return opportunities. Below was my initial research report on the company. If the stock gets into our buying zone, we’d be more than willing to buy again if we deem it to be the best opportunity!

AGCO Corp.: Cyclical Downturn in Farm Incomes Creates a Buying Opportunity (Nov. 2014)

Summary

- Short-term concerns and a cyclical downturn have created a buying opportunity for AGCO.

- AGCO boasts a tremendous geographical footprint and is one of the three leading farm equipment manufacturers.

- At current prices, AGCO is an attractive acquisition target for a merger, buyout, or the common shareholder.

Because most market participants are focused on the short term, long-term investors have the ability to take advantage of a time arbitrage of sorts. Industries and companies that are likely to struggle in the next quarter or year are often offered at cheap prices, despite the fact that the long-term outlook might be quite favorable. Intelligent businessmen often take advantage of this by looking to acquire companies in cyclical downturns, so as to take advantage of the reduction in price due to short-term headwinds, when the intrinsic value is likely to be materially higher. Such an opportunity exists right now in the farm equipment sector and specifically in the common stock of AGCO Corp. (NYSE:AGCO). Short-term concerns over farm income and a cyclical decline in earnings, have caused the stock to sell off to where it can now be acquired at a 35-50% discount to our estimate of intrinsic value.

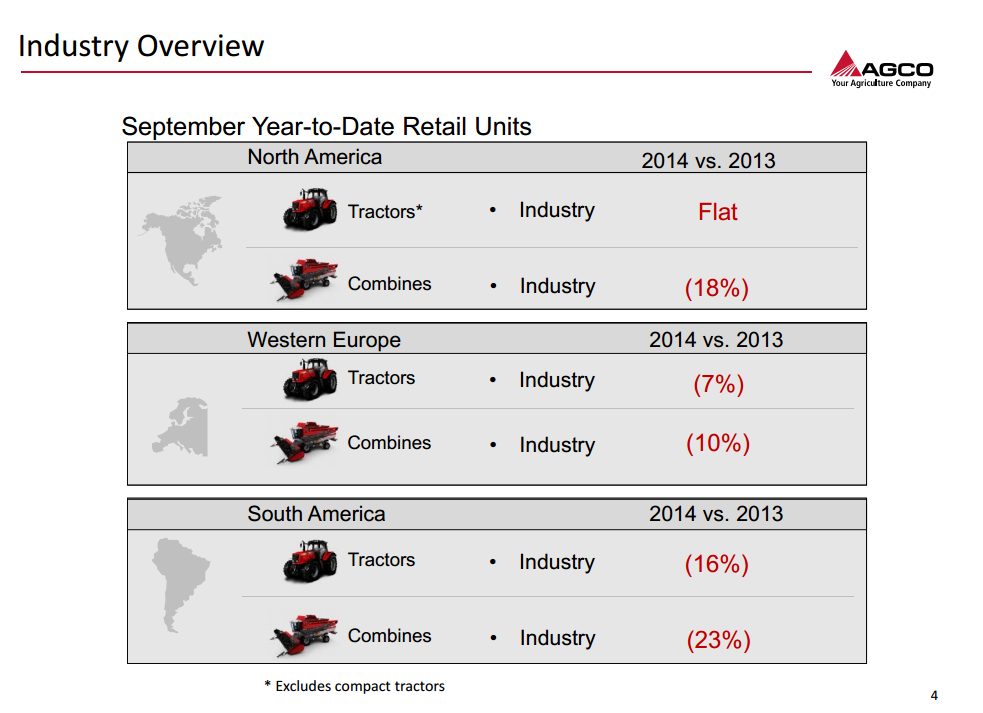

The last decade has been enormously favorable for the farm equipment industry. Regulations requiring certain levels of ethanol production and, more importantly, an increasing demand for food from emerging economies have led to increasing prices and incomes for farmers. Increased incomes have enabled strong profit growth for the large farm equipment manufacturers. Commodities are always cyclical, and favorable weather conditions across the globe have led to excess supply in major crops such as corn and wheat. The excess supply in most crops has obviously reduced farm incomes, pressuring demand for farm equipment and has led to decreased earnings for the farm equipment manufacturers.

AGCO boasts a tremendous geographical footprint and is one of the three leading farm equipment manufacturers. The company makes tractors, combines, self-propelled sprayers, hay tools, forage equipment, grain storage, protein production systems etc. Some of the company’s leading brands are Challenger, Fendt, GSI, Massey Ferguson and Valtra. AGCO’s products are distributed through a combination of approximately 3,100 independent dealers and distributors in more than 140 countries. Tractors are the company’s biggest seller, accounting for 60%, 59% and 66% in 2013, 2012 and 2011, respectively. Hay tools, engines, and forage equipment are the second largest product line, generating 9% of sales. Replacement parts account for about 13% of sales. AGCO also owns 49% of a retail finance joint venture with Rabobank.

{kind=link}

{kind=link}

Net Sales and Operating Margins

{kind=link}

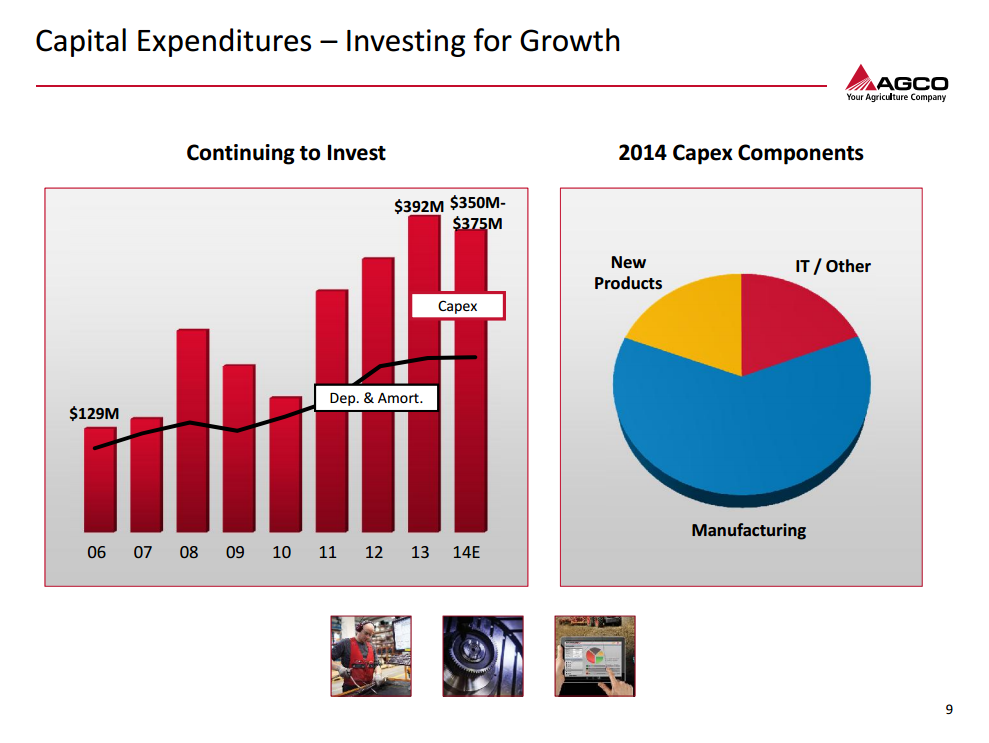

Capital Expenditures – Investing for Growth

{kind=link}

AGCO has nearly 50% market share in Brazil, which is a huge and growing agricultural market, but the farm equipment industry in Brazil is about 1/4 the size of North America, where Deere (NYSE:DE) is dominant. The company is also strong in Europe and the Middle East. AGCO owns 23% of TAFE, which is the 2nd largest tractor manufacturing firm in India after Mahindra & Mahindra. This could be an underappreciated source of value, in that the stake is valued based on purchase accounting and growth has been strong. Returns on invested capital have been about 10% over the last decade, but we acknowledge that returns are likely to decline slightly over the next decade, particularly if we see decreased subsidies for ethanol production.

While these are a few of the strengths, AGCO also has some characteristics that are disadvantageous. The company’s assortment of brands leads to a diluted marketing approach versus the likes of Deere. AGCO splits roughly $60 million across its 4 major brands, versus Deere which does about $200MM in advertising on its primary brand. Because of the variety of brands, the dealer network is not nearly as cohesive or well-promoted as it leading competitor. AGCO also would benefit from owning 100% of its financing unit as opposed to 49%; because the company doesn’t have the same control over the customer relationship, or retain the ability to enhance promotional activity to pursue market share when necessary without having full ownership.

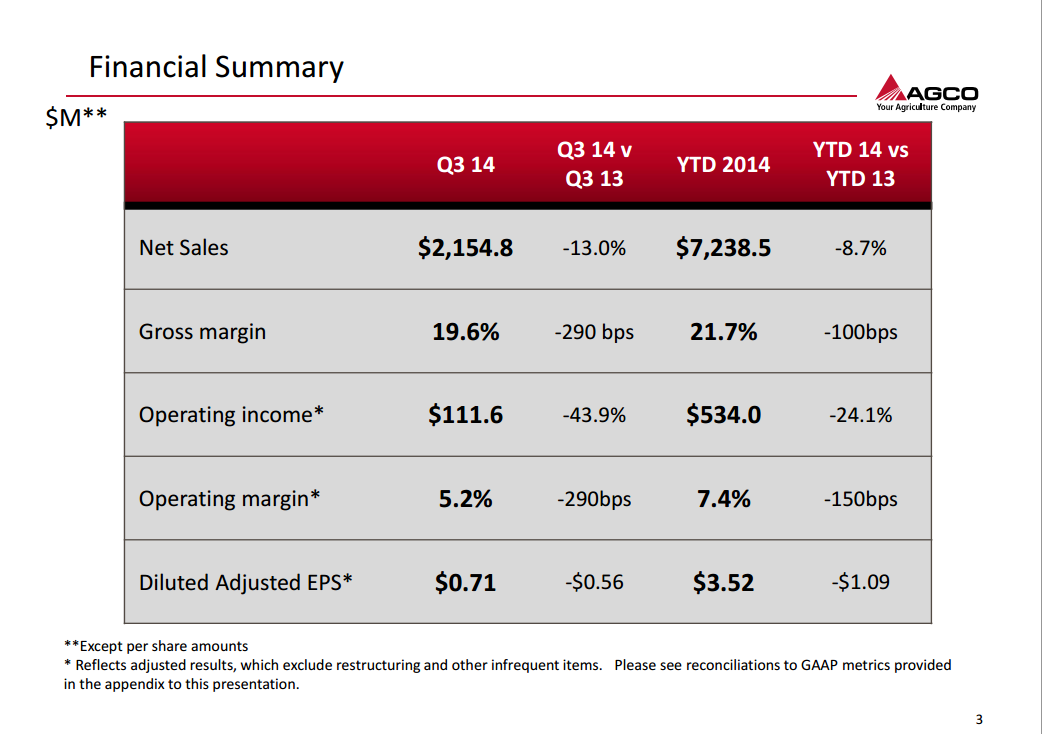

On October 28th, AGCO reported 3rd quarter earnings. Sales of $2.2 billion were down 13% YoY, while net income was $0.69 per share and adjusted net income, excluding restructuring and other infrequent expenses, was $0.71 per share for the 3rd quarter of 2014. These results were down from reported and adjusted net income of $1.27 per share in the same quarter last year. For the first nine months of 2014, reported net income was $3.50 per share and adjusted net income, excluding restructuring and operating expenses, was $3.52 per share. These results were down from reported and adjusted net income of $4.61 per share in the first 9 months of 2013. Full year earnings per share guidance is $4.10 to $4.30 for the year, down from $6.01 per share in 2013. Inventories grew by about 15% to $2.3 billion, so AGCO is now taking action to aggressively reduce production.

At the end of 3rd quarter, AGCO had 93.8MM shares outstanding. At a recent price of $44.41, AGCO has a market capitalization of roughly $4.166 billion. The company ended the quarter with about $1.333 billion in long-term debt, which was partially offset by $321MM in cash and cash equivalents. The enterprise value is roughly $5.2 billion for a company that generated approximately $500MM in free cash flow in 2013. Admittedly, free cash flow is sporadic and is declining to about $125MM-$150MM in 2014, but the earnings power of the company is quite a bit higher than current performance would insinuate. Trailing twelve month EBITDA was roughly $990MM, so the EV/ TTM EBITDA is about 5.25, which is quite cheap for a solid global franchise operating at near-trough conditions. Deere in comparison trades at approximately 9.18 on an EV/TTM EBITDA basis. AGCO has earned over $5 per share in each of the last 3 years, so as the cycle improves, AGCO could likely have $7-8 per share of earnings power by 2016-2017.

I believe that a sophisticated buyer such as a Caterpillar (NYSE:CAT) would be willing to pay $60-$65 to acquire AGCO. This would enable Caterpillar to compete with Deere in its farm equipment unit just as Deere competes with Caterpillar on construction. There would be numerous synergies from the acquisition in terms of procurement and dealer realignment. I also believe that Caterpillar would be able to utilize its own captive financing unit, which would bolster AGCO’s competitive position, in addition to boosting the advertising spend and R&D budget.

Private equity is also a potential buyer of AGCO, but even if the company stays independent, I believe the stock is worth materially more than the current share price would indicate. The company has bought back about 6% of its common shares outstanding over the last 9 months and insiders have been buying aggressively. Long-term investors would be wise to follow their lead to take advantage of this well-financed global manufacturer before cyclical conditions improve, as by that time the stock will likely be closer to $60 on the conservative side.

As always, if you have any questions whatsoever please don’t hesitate to call me at 805-886-8140.