Dear Investors,

Equity markets are in a bit of a tailspin of late given concerns about the uncertainty of trade negotiations. Amazingly, financial stocks have declined a record 13 days in a row, which is creating some interesting value opportunities in the space. As I’ve discussed before, I’m not overly concerned about the issue of trade, as it is in everyone’s interests to work out a deal that works for all parties. However, I’ve had concerns about the overall market for a longtime, as valuations are near all-time highs. There is often a lot of talk about value underperforming growth. That hasn’t been our experience since inception, especially when you consider our lower risk profile, and I often question what constitutes value stocks in such broad-based terms. It is interesting though that the valuation spread between value and growth stocks is the highest that it has ever been. That is very reminiscent of 2000-2003, when markets tanked, but value stocks rallied like crazy. Most of our securities trade at discounts to book value and have been buying back stock at large discounts to intrinsic value. That is enormously bullish long-term.

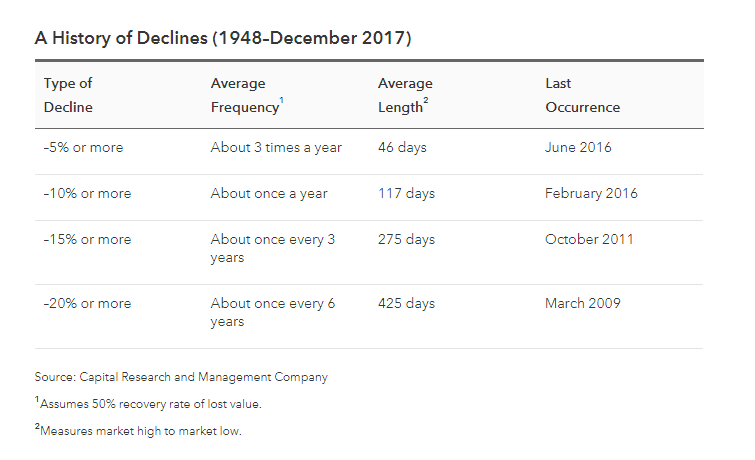

Below is a helpful table produced by American Funds on market declines. As you can see 5% declines are expected about 3 times a year. A 10% decline occurs about once a year. A 15% or greater decline occurs about once every 3 years. Lastly, a 20% correction occurs about once every 6 years. While markets are rather erratic right now, I’d like to remind you that it has been just about exactly 2 years since the Brexit vote shattered market confidence. It is about 19 months since the Presidential election shocked the world and economists such as Paul Krugman were basically calling for the next Great Depression. Both of those proved to be huge buying opportunities. I’m not saying that is the case today for the overall market, but I don’t think it is the end of the world either.

Our portfolios have a lot of different layers of protection. Many of our stocks have huge dividend yields, which produce steady streams of cash flow. We utilize cash-secured puts and covered calls to enhance income, reduce risk, and to manufacture cheaper entry-prices into stocks. If we end up getting exercised on some of them, we have a great chance of making 50-100% over the next 3-5 years as the stocks recover.

I wouldn’t invest a dollar in index funds at present valuations. Markets have had multiple decade-plus occurrences where returns were negative. People seem to forget that from the market top in 2000 until October 2002, the S&P 500 index had dropped by half, and the technology-heavy Nasdaq 100 Index had lost 80%. Bitcoin is down roughly 70% YTD. Paying too much is a financial death sentence in financial markets and we go to great lengths to avoid doing so. That doesn’t mean our stocks won’t drop from time to time, but usually that turns out to be a great buying opportunity, as long as the fundamentals aren’t materially changed.

Much of the financial advisory industry has become obsessed with index funds. Vanguard (my old employer) is printing money like it is nobody’s business. However, many of these market participants didn’t get into index funds in 2009 when the market bottomed, or even 2012. Fund flows have picked up dramatically as the market valuations have increased. That is not intelligent investing. There is no doubt that there are a lot of terrible asset managers that index funds can outperform over the long-term. It is important to see a full market cycle though, which includes a bear market/recession. Most retirees for instance aren’t comfortable being 100% long stocks like you are in an index. If you own the QQQ, can you afford a 50-60% drawdown, which is not impossible and is in fact very likely at some point? Just as bad is the fact that index funds are being misrepresented. People are acting as though they are going to hold them forever. Yeah right!

According to research from Michael Batnick, since March 2009 to August 2016, investors in the largest S&P 500 ETF, SPY have underperformed the fund by 115%. That is a staggering number but just about every fund has similar dynamics. The reason why it occurs is simple. Market participants get scared away when pessimism hits and they sell their stocks, only to buy back again at higher prices when optimism once again reemerges.

It is our nature to think we can time the market. Many market participants think that they can ride the wave but get out before it crashes. That isn’t realistic whatsoever and nobody has done that successfully over a long-term time horizon. Volatility is a guarantee when we invest in stocks. Taking advantage of volatility instead of being scared by it is one characteristic that separates good investors from bad ones. One of the primary reasons I believe we have unique clientele at T&T Capital Management is that our clients aren’t generally the type that panic. They are well-educated and understand that we are focused on the long-game.

We spend a lot of time on communication because we want you to understand your positions and understand the strategy behind them. I’ve seen clients miss out on millions of dollars by panicking and it is like a stake through the heart when it happens, but fortunately those instances are very rare for our client-base, but they are quite common at most other firms. Below is our most recent research report on Brighthouse Financial, which was recently spun-off from Metlife. The stock trades at roughly 38% of book value as it has been under pressure as Metlife has divested its stake.

I hope that you enjoy and as always, if you need anything at all, please don’t hesitate to contact me or Peter directly. Peter’s number is 949-734-4290 and mine is 805-886-8140!

Future Prospects Brighter For Brighthouse Financial

Sincerely,

Tim Travis