One stock that we’ve been buying over the last few months is an international real estate development firm called Kennedy Wilson (KW). KW has a large presence in Multifamily and Office real estate in mostly the western United States, the UK, and Ireland. Management takes pride in being a value investor through acquiring opportunistic investments and fixing them up. The company devotes most of its capital to buying buildings with a focus on maximizing property cash flow. KW also raises 3rd party capital from institutions and invests in real estate development globally, which brings in fee revenue and leverages its purchasing power.

KW was a very early investor in key markets such as Seattle, Washington and Dublin, Ireland. These are two very fast-growing markets with Seattle benefitting from the continued rise of companies such as Amazon and Microsoft, while Dublin is becoming a leading EU destination for global corporations in the midst of the Brexit. KW is not a REIT, which means that it is a full taxpayer at the corporate level. The company is not covered by many analysts, which I believe plays a part in the disconnect between price and value.

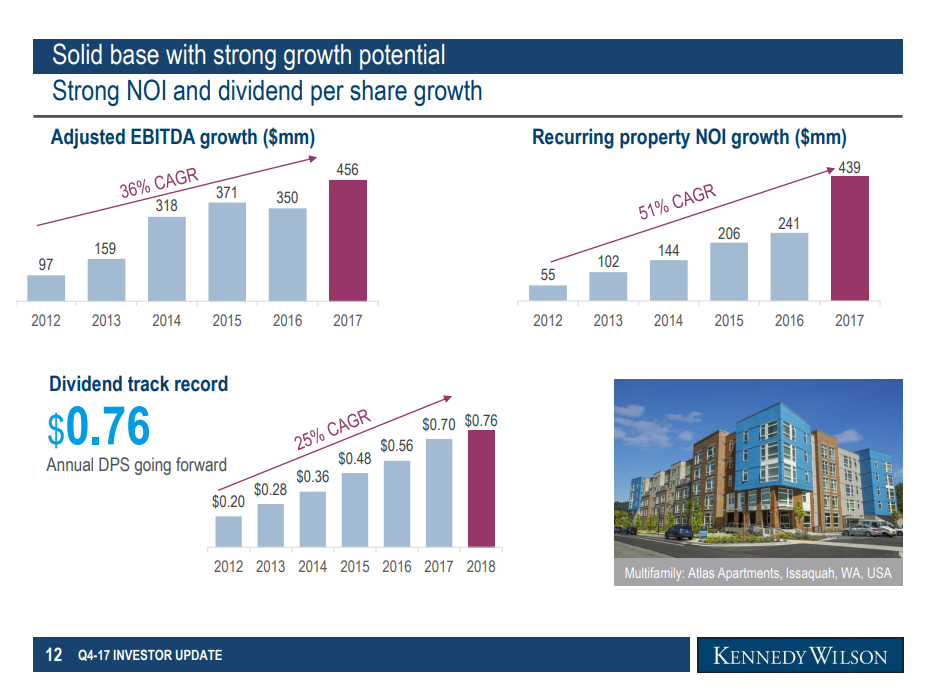

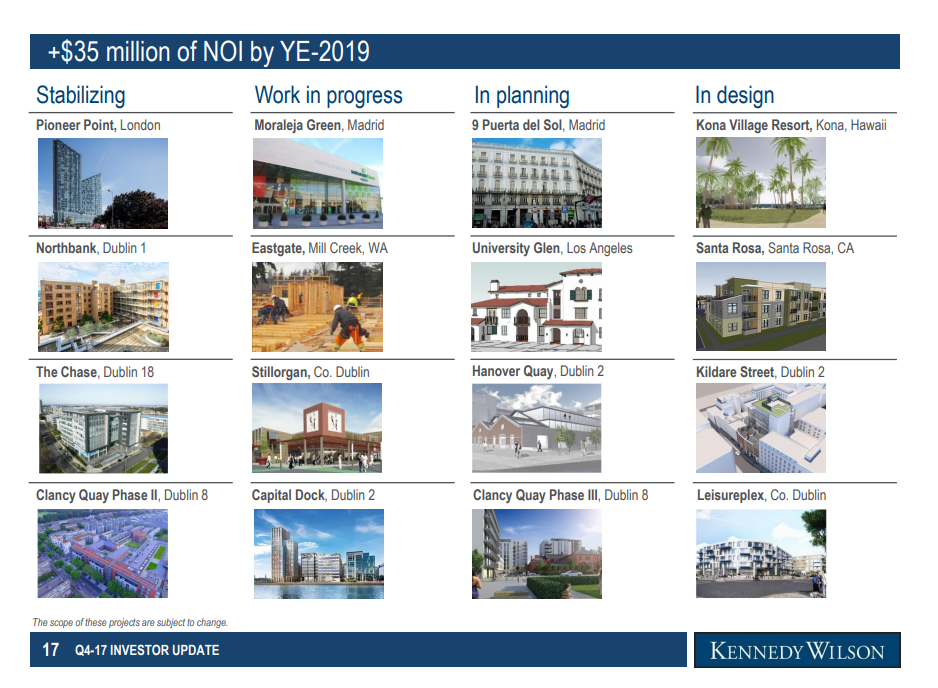

The company has dramatically increased its net operating income over the last several years. It estimates its current annual net operating income at $439MM, with a plan in action to grow net operating income to $474.1MM by the end of 2019. In addition to it income-generating properties, KW has about a billion dollars invested in unstabilized development and non-income producing assets. Much of this was bought for very low prices and the current strategy is to sell parts of it to focus the balance sheet on enhancing net operating income.

On March 20th, the company announced a $250MM stock buyback based on the proceeds of some noncore asset sales. This is a very positive development for shareholders as KW is deeply undervalued. There is nobody that understands KW assets better than KW management, so by buying its own stock at a huge discount, the company is finding better value than they can in the real estate market. The stock pays a dividend of 4.4% and we believe the stock should ultimately increase from around $17 to $30 over the next 2-3 years. Insiders own 13% of the stock and it wouldn’t be impossible to see a buyout if the stock continues to languish. The $250MM buyback should allow the company to buyback approximately 10% of shares outstanding based on recent prices, which should be highly accretive. As investors, we love when management take advantage of the disconnect between price and value by buying back stock aggressively. Alternatively, we very much dislike when companies buy back stock at a premium to intrinsic value, which is what many of the companies in the S&P 500 are doing right now.

“There is nobody that understands KW assets better than KW management, so by buying its own stock at a huge discount, the company is finding better value than they can in the real estate market.”

We believe that we can offer considerably more protection than the overall market by focusing on individual securities, as opposed to broad-based index purchases with the market at such an expensive valuation. Investing and wealth creation take patience and time. The process is not different than KW buying a building when it is out of favor, fixing it up, and selling it in more fortuitous circumstances. At the height of a bull market, market participants tend to think that returns will simply continue to be strong even when the math tells a very different story. We must train our brains to think very differently and not stray from a focus on price and value. This is precisely the lesson that Benjamin Graham learned from his experiences investing during the Great Depression, when almost everyone investing was going bust. This method of value investing has stood the test of time for nearly 100 years, but the basic business logic of it goes back much further of course. It can be uncomfortable positioning ourselves differently than everybody else, but it is only in doing so that we can avoid the same pitfalls that devastated market participants in 2000 and 2008, and will likely do so again as this speculative mania comes to a head.

“We believe that we can offer considerably more protection than the overall market by focusing on individual securities, as opposed to broad-based index purchases with the market at such an expensive valuation.”

Below are some slides that go into a little more detail about KW’s operations and we’ll continue to keep you updated on developments for the firm. As always, if you need anything at all, please don’t hesitate to contact us!

Kennedy Wilson Announces $250 Million Share Repurchase Program

Sincerely,

Tim Travis