Dear Investors,

Military history is riddled with examples where generals and nations were woefully unprepared for battle, due to their ill-founded notions that the next war would be the same as the last. A great example of this was World War 2. The French built the Maginot Line, which was an extensive network of concrete fortifications and weapon installations, that was built to deter Germany from invading again. The Maginot Line was built on French borders with Italy, Switzerland, Germany, and Luxembourg. Most experts thought that the Maginot Line was invulnerable to aerial bombings and tank fire.

However, during WW2, the Germans simply bypassed the Maginot Line by invading through the Low Countries. This was not unexpected by the French and British who planned to aggressively counterattack through Belgium, but their line was vulnerable near the Ardennes forest, where the brutal terrain was believed to make an attack highly unlikely. The German’s utilized their Blitzkrieg attack to storm right through the forest, assisted by the technological advancements that had occurred in the weapons of war such as tanks and planes. Ultimately of course, France was conquered in a shockingly short period of time, setting the stage for the dramatic Dunkirk escape to salvage the British war effort.

The reason that I bring this up is because many investors tend to believe that the next major bear market will occur the same way that the last one did. The Great Recession was headlined by declining housing prices and the collapse of our financial system, best embodied by the bankruptcy of Lehman Brothers. When we have seen major volatility over the last few years via Brexit, oil’s rapid drop in early 2016, or the European Sovereign Debt Crisis, U.S. banks sold off aggressively. Just the past few weeks, financial stocks were down 13 days in a row as fears of trade uncertainty superseded strong fundamentals in the minds of traders.

I believe that the dominance of ETFs and high-frequency trading likely has a lot to do with how highly correlated financial stocks tend to be with increasing volatility. For long-term investors, these short-term selloffs tend to open up attractive opportunities. We’ve taken advantage of the disconnect between price in value in all of those major market events and it has paid off. The banks have rallied a lot and while we still have positions in them, they are not the major catalyst in our portfolios’ anymore, except for ALLY.

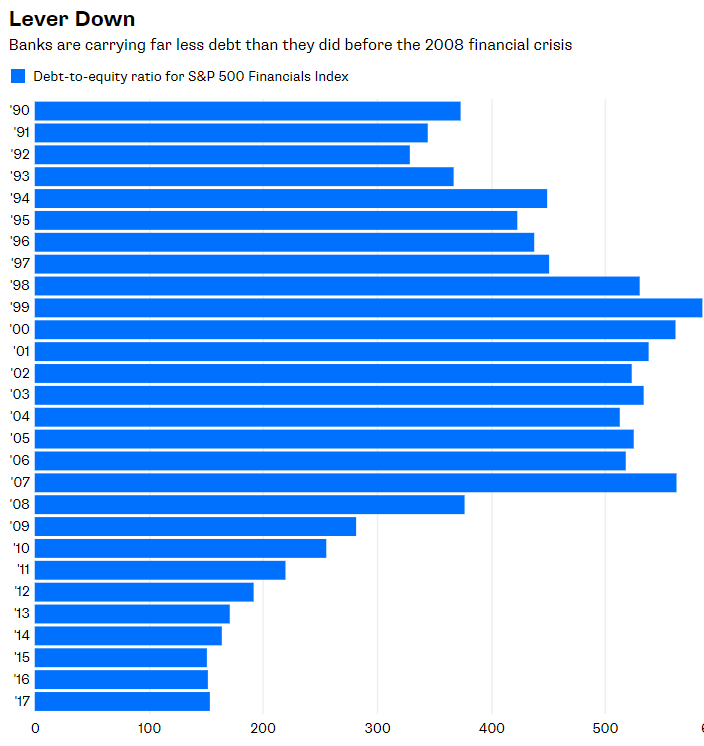

Yesterday, the CCAR results were released, which dictate how much capital the banks can return to shareholders via dividends and stock buybacks. The banks that we have positions in all came out very well and announced increased dividends and stock buybacks. ALLY for instance, raised its dividend and announced a $1 billion stock buyback, which is nearly 10% of the market cap. With the stock trading at less than tangible book value and at a single-digit forward P/E, these buybacks are enormously accretive. Our banking system is the safest it has been in many decades, if not ever. Capital and liquidity ratios have doubled. Returns on equity are lower due to this, but that is a fine tradeoff because you have dramatically safer enterprises that can weather the next financial storm.

I think it is much more likely that the next major market correction will have a very different catalyst than the last crisis. It could very well be stock valuations, which are at some of the highest levels in history. While it seems unlikely based on current sentiment, the big tech stocks such as Apple, Amazon, Facebook, and Google have gotten so big that if they were to decline materially, that could easily drive an exodus out of many funds that hold them in great size. Selling begets more selling, as market participants panic. Maybe inflation will perk up and force the Fed to raise rates faster than expected. Perhaps China’s expansion and credit bubble will finally pop having a global impact. The truth is, none of us know for sure what will cause the next bear market. As investors, we must focus on what we can do.

We perform extensive research on each and every security that we own. If the stock sells off without a change in the fundamentals, that is almost always a great opportunity. If we didn’t know the companies inside out, we could not do that. Many market pundits say that if a stock declines by x percentage, you should sell not matter what. That is absolutely asinine if you have any concepts of the actual underlying business value, but unfortunately many advisors do not.

We use conservative tools such as cash-secured puts and covered calls to reduce risk and generate cash. These strategies might hurt us in a year like 2017 when markets go straight up, but they provide significant protection when markets take a turn for the worse. Just as importantly, we are invested in a variety of special situations. AGO and AMBC for example, are likely to be driven more by legal events than general market sentiment. We have a large margin of safety in them in which we don’t need everything to break our way to be very successful with them.

Below is a great article from Bloomberg that inspired this newsletter topic. All of these sites seem to have paywalls now, so I’m not sure if you can read it or not but it is worth your time if so. Thank you very much and let us know if you need anything at all!

Forget Banks and Worry About High Stock Prices

Sincerely,

Tim Travis